9 Steps to Understanding PG&E’s Roth 401(k) Options: How to Build a Tax-Smart, and Life-Smart Retirement Savings

Learn how PG&E’s Roth 401(k) options, conversions & after-tax features boost tax-free retirement income. See key rules, limits & strategies for a smarter plan.

%20Options.avif)

PG&E employees now have more flexibility than ever when saving for retirement. With new Roth 401(k) features, expanded contribution limits, and the ability to convert savings inside your plan, you can choose when and how you pay taxes on your retirement money.

1. The Basics: Traditional vs. Roth 401(k)

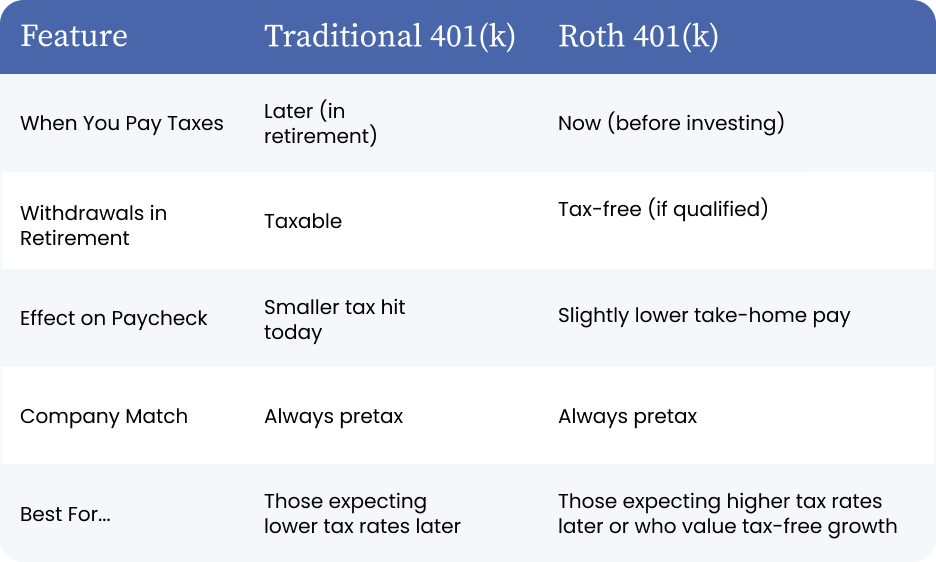

The traditional 401(k) has been around for decades. You make pre-tax contributions, which lower your taxable income today. You’ll pay taxes later when you take money out in retirement.

A Roth 401(k) works the opposite way: you contribute after-tax dollars, pay the taxes now, and your future growth and withdrawals can be completely tax-free if the rules are met.

PG&E still matches Roth contributions the same way it matches pre-tax ones, but that match is always deposited pre-tax. You’ll owe taxes on it when you eventually withdraw it.

2. Why Roth Matters More Now

PG&E’s new Roth 401(k) option is available to both management and union employees. Starting in 2026, union employees will be able to contribute up to 50% of their pay (up from 20%). Still subject to contribution limits.

That means more opportunities to build tax-free retirement income and more decisions about how to split contributions between traditional and Roth accounts.

The big question:

Should you pay taxes now (Roth) or later (traditional)?

There’s no one-size-fits-all answer. It depends on your income, tax bracket, and retirement goals.

A PG&E Example: Sam and Rosa

Let’s look at two coworkers.

Rosa, 45, makes $150,000 and expects her retirement income to be lower. She prefers the traditional 401(k) because it reduces her taxable income today and aligns with her current budget.

Sam, 28, earns $90,000 and expects his income to rise. He chooses the Roth 401(k), paying taxes now while rates are lower, so his withdrawals are tax-free later.

Both are smart decisions. They’re just using the option that fits their situation.

3. Tax Diversification: The Best of Both Worlds

You’ve heard of investment diversification; tax diversification works the same way.

By splitting contributions between traditional and Roth accounts, you give yourself flexibility in retirement.

- If tax rates rise, pull from the Roth side to avoid extra taxes.

- If you want to deduct contributions while working, consider contributing to a traditional plan.

- In retirement, consider mixing and matching withdrawals to minimize your taxable income. (Tax Diversification)

It’s like having two gas tanks for your financial journey; you can choose which to use based on the road ahead.

Feeling lost or needing support for your PG&E 401k, or planning for your retirement. Reach out to us, we work with individuals in the PG&E retirement field everyday, and want to help you retire well.

4. How a Roth In-Plan Conversion (RIPC) Works

PG&E’s plan extends beyond simply choosing between a pre-tax and Roth option. You can convert existing pre-tax or after-tax savings into your Roth 401(k) account.

Here’s how it works:

- Pre-tax money and earnings are taxable in the year you convert.

- After-tax contributions aren’t taxed again, but their earnings are.

- Once converted, all future growth is tax-free if you follow the 5-year and age-59½ rules. (Next week’s post will address this topic)

You can even automate this through “spillovers”, once you hit the IRS contribution limit ($23,500 plus $7,500 catch-up for age 50+), extra after-tax contributions can automatically convert to Roth. The spillover is sometimes referred to as a mega backdoor Roth and is a powerful way to build tax-free wealth.

5. After-Tax Contributions: The Hidden Advantage

Most people stop saving once they hit the regular 401(k) limit, but PG&E allows you to go further.

After-tax contributions allow you to save up to the total plan limit of $70,000 (including the match).

If you enable the in-plan conversion feature, those after-tax dollars can be automatically moved into a Roth account, turning potential future tax bills into tax-free income.

This strategy is particularly useful for higher-income earners who have already maxed out their regular 401(k) and want to continue compounding wealth efficiently.

6. The 2026 Catch-Up Rule You Can’t Ignore

Starting in 2026, anyone who earned more than $145,000 in the prior year must make all catch-up contributions as Roth.

If that applies to you, you’ll need to update your election, or your catch-ups will stop automatically.

If you earn less than $145,000, you can still choose between pre-tax and Roth for catch-ups.

This rule makes Roth awareness even more critical for higher-income PG&E employees nearing the end of their careers.

7. The Tax Side of Converting

When you convert funds to a Roth:

- You’ll owe ordinary income tax on pre-tax amounts converted.

- You’ll owe tax on earnings from after-tax contributions, but not on the original after-tax dollars.

- You’ll receive an IRS Form 1099-R showing the taxable amount.

PG&E and Fidelity don’t withhold taxes automatically, so plan ahead. Set aside cash or adjust withholding elsewhere so you’re not surprised when filing your tax return.

8. When a Conversion Makes Sense

Ask yourself three questions:

- Do you expect higher taxes in the future?

- Paying now might save you later if your income or tax rates rise.

- Do you have time on your side?

- The longer your money can grow tax-free, the more powerful a Roth becomes.

- Can you pay the taxes from outside the plan?

- Using non-retirement funds to cover the bill keeps more invested and compounding.

Conversions aren’t all-or-nothing; you can convert just your after-tax contributions or do it in stages over several years, filling your current tax bracket. Referred to as bracket-filling or serial Roth Conversions.

9. Roth 401(k) vs. Roth IRA: What’s the Difference?

Both grow tax-free, but they play by different rules.

%20vs%20Roth%20IRA.png)

If you’re eligible, you can do both, maxing out your Roth IRA and your Roth 401(k) for even more tax-free growth potential.

How to Get Started

To set up or convert inside in your PG&E benefits, call Fidelity at 1-877-743-4015. They’ll confirm your account details and walk you through enabling Roth contributions or the in-plan conversion feature. There’s no fee for conversion transactions.

Then, review your plan annually, especially as the 2026 catch-up rule approaches, to make sure your strategy still fits your tax picture and goals.

PG&E’s 401(k) now offers more flexibility, more control, and more opportunity than ever to shape your financial future.

Whether you use traditional, Roth, after-tax, or a mix of all three, the goal is simple: build a tax-smart plan that funds the retirement you actually want to live in.

At Powering Your Retirement, I help PG&E employees determine when and how to utilize Roth strategies, ensuring their retirement plan isn’t only tax-smart but also life-smart.

If you’d like to see how a Roth strategy fits into your overall plan, schedule a time to review your situation. As a Certified Financial Planner™ and Enrolled Agent, I integrate your investments and taxes into a single, clear strategy, allowing you to focus on your days, not your dollars.

P.S. I try not to be too promotional in these posts. This week, please share this article with your coworkers if you hear someone talking about the new Roth options. My goal is to inform as many PG&E employees as possible.

Powering Your Retirement is a Registered Investment Advisor. Registration as an investment adviser does not imply a certain level of skill or training, and the content of this communication has not been approved or verified by the United States Securities and Exchange Commission or by any state securities authority. The information contained in this material is intended to provide general information about Powering Your Retirement and its services. It is not intended to offer investment advice. Investment advice will only be given after a client engages our services by executing the appropriate investment services agreement.

You May Also Like,

Here are some must-read blogs you don’t want to miss! Get expert tips on retirement benefits, 401(k) management, and more. Stay in the know and make the most of your retirement planning!

Are You Ready for Retirement?

Book your free, no-strings-attached assessment—a stress-free process where we’ll tell you the exact amount you need to retire, when you want to!